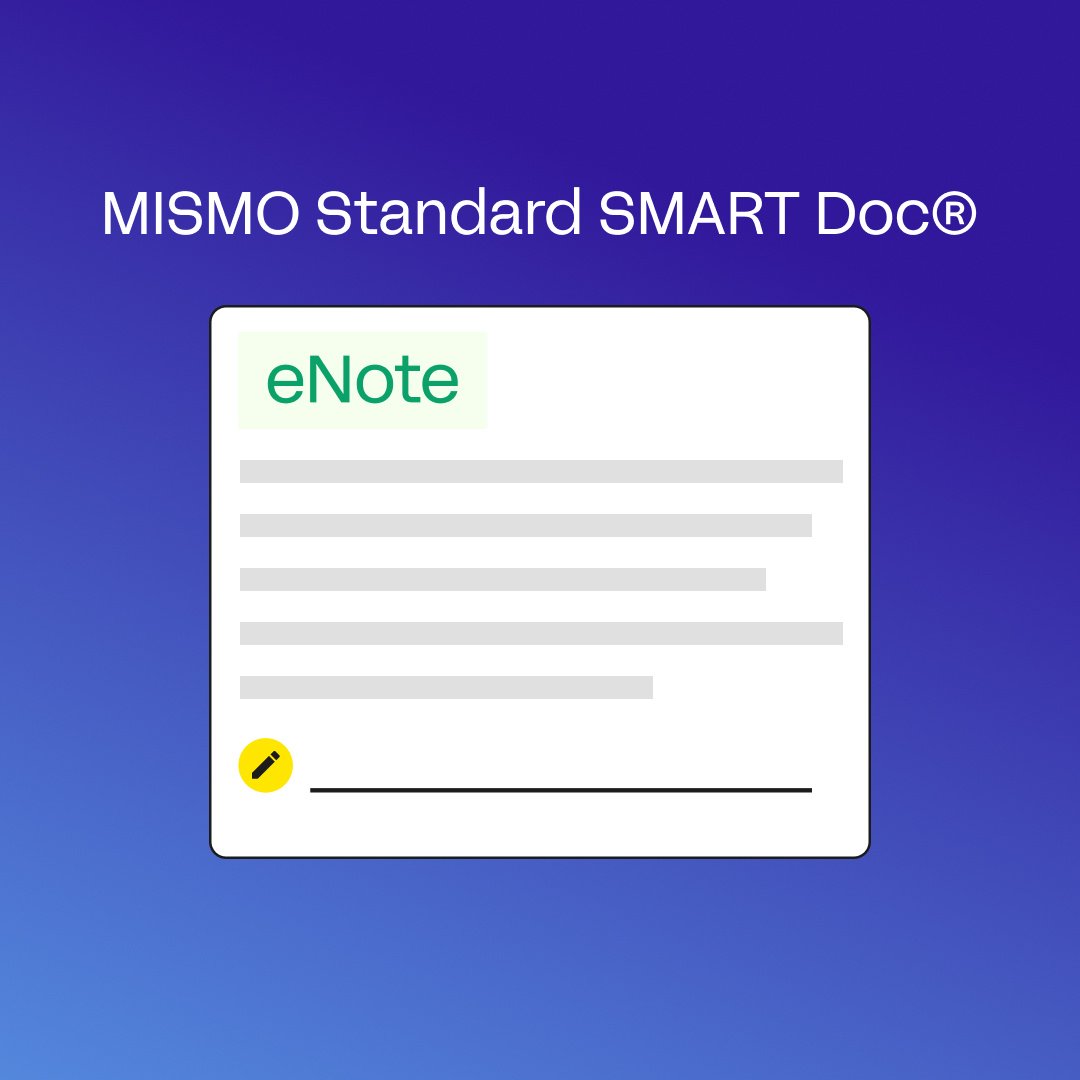

Step 1: The eNote is created

The eNote is created by the eVault, in accordance with the MISMO Standard SMART Doc® format for electronic documents.

Step 2: The borrower eSigns the eNote

The borrower electronically accesses, views, and eSigns the eNote via the lender’s eClosing solution.

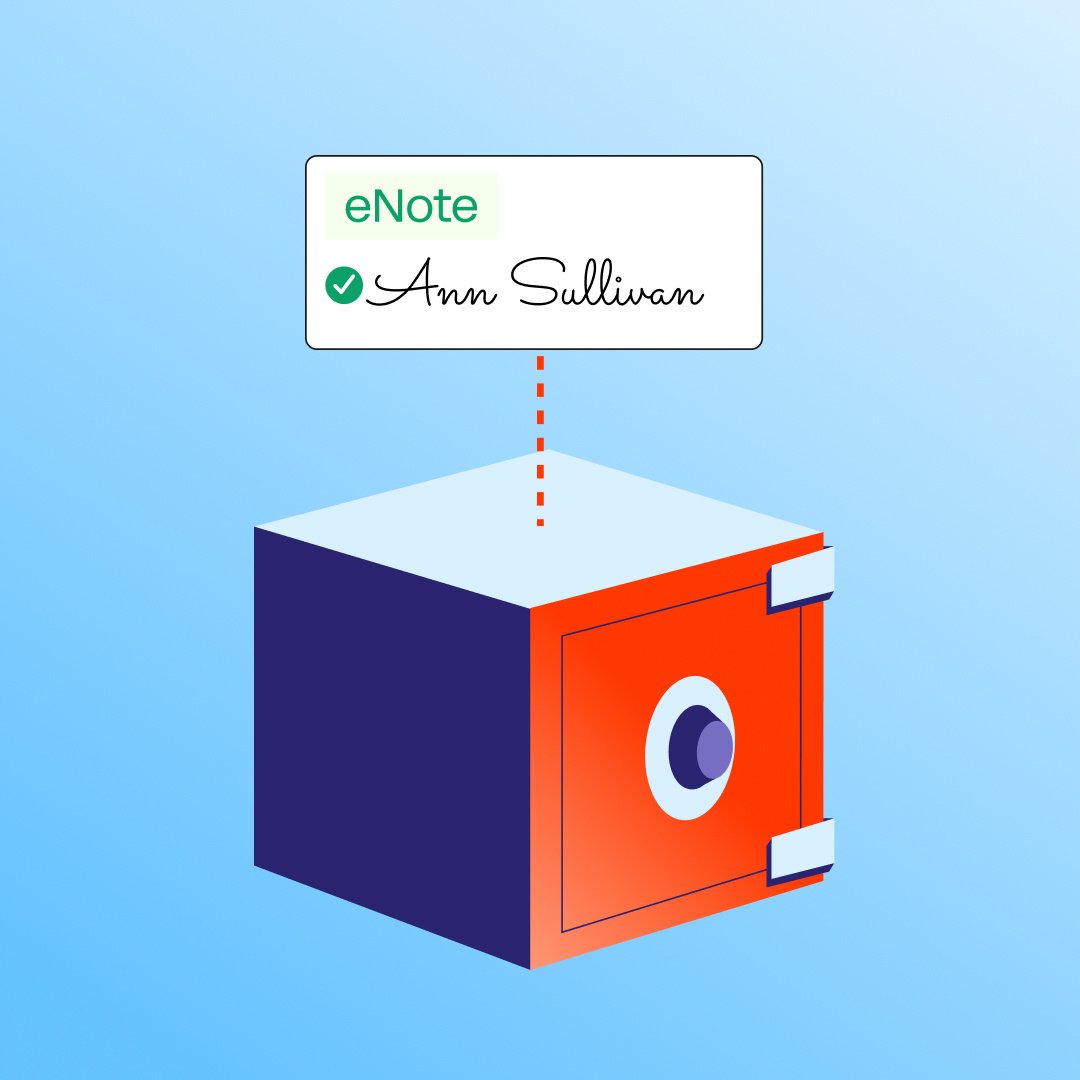

Step 3: The eNote is securely stored in the eVault

After the borrower has eSigned, a tamper-evident seal is applied to the eNote and it is automatically stored within the eVault.

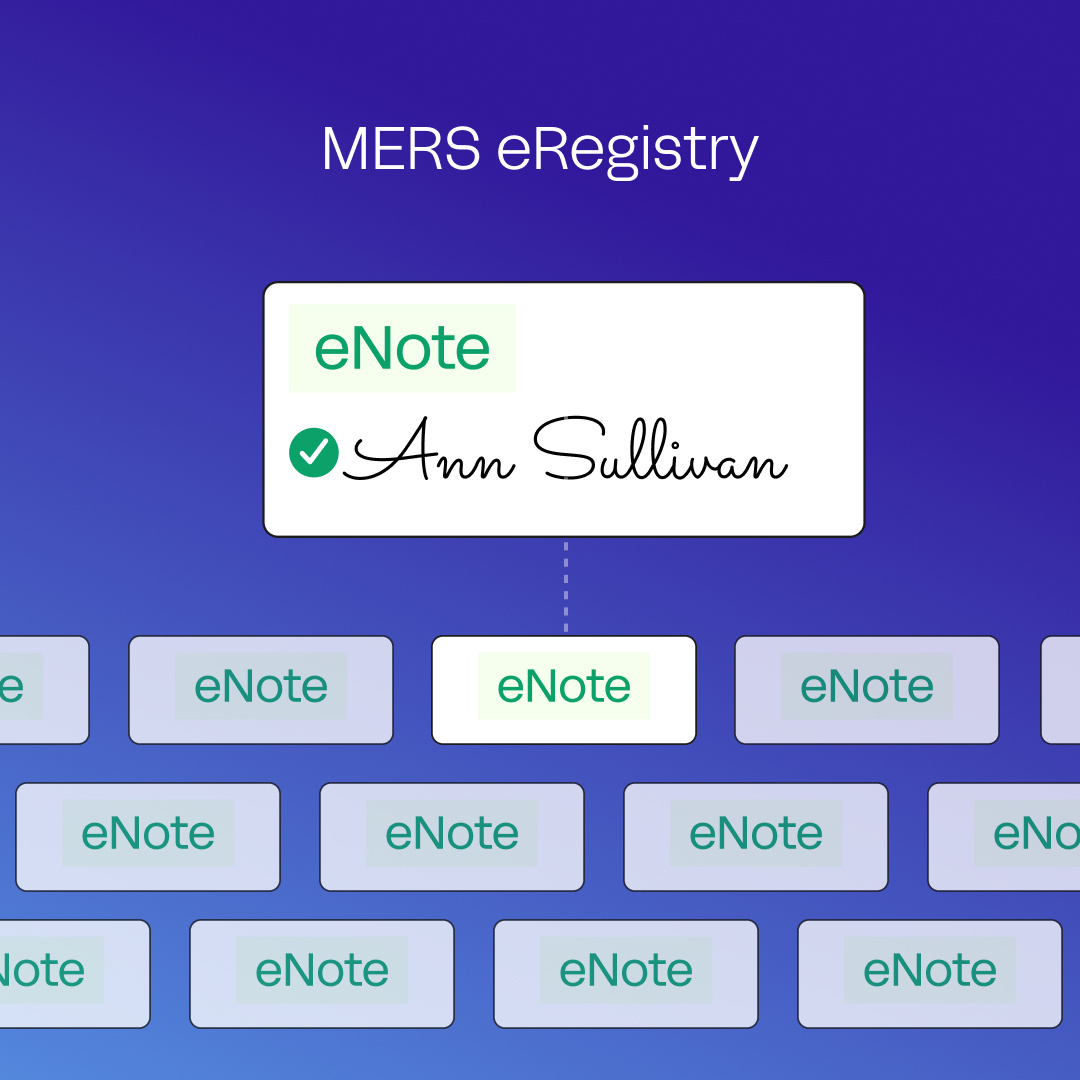

Step 4: The eNote is registered

The eNote is automatically registered on the MERS® eRegistry—the system of record that verifies eNote rightsholders.

Step 5: The eNote is delivered to the secondary market

Once the eNote is sold, a copy of the eNote is transferred to the trading partner’s eVault via MERS® eDelivery.

The right eNote strategy

Lenders have diverse eClosing needs. Our team has developed tailored eClosing strategies to meet the unique requirements of each customer.

Award-winning support

We're committed to your success from day one. Our team is known for delivering white-glove implementation, onboarding, training, and change management support.

Specialized technology

Our specialized solutions have helped hundreds of lenders scale eNote adoption at rates 2x higher than industry average.

“eNotes reduce reputational risk because we do not have to go back to the borrower for corrections. It’s also a much more efficient process, which is better for our relationships with investors and warehouse lines. We're seeing better pricing and stronger partnerships overall. The return on investment is endless.”Alyssa North, SVP of Operations

eNote FAQ

eNote FAQ

Q: What are the benefits of eNotes?

There are significant benefits of eNotes for mortgage lenders, primarily when it comes to security, cost-savings, and secondary market efficiency:

Realize more value per loan

Achieve an average savings of $2151 per loan with eNotes—thanks to improvements in operational and secondary market efficiencies.

Eliminate the need for manual shipment and storage of paper promissory notes, reducing both the time and costs associated with preparing and shipping physical documents.

Secure storage for the life of the loan

eNotes are digitally stored and transferred between parties. This means eNotes cannot be damaged, lost, or tampered with—and ensures the enforceability of the note throughout its lifetime.

Increase control of time spent on warehouse lines

Because eNotes are digital documents, lenders are able to expedite (and control) loan delivery to investors—while accelerating access to capital.

1 Savings calculations were independently conducted and verified by Falcon Capital Advisors, based on the analysis of 15 lenders' pre- and post-eClose workflows

Q: Which investors accept eNotes?

Investor acceptance of eNotes is steadily increasing. Fannie Mae, Freddie Mac, Ginnie Mae, and Mr. Cooper are among the many organizations that accept eNotes today. For an updated list of all companies that accept eNotes, visit the MERS eRegistry.Q: What is the difference between a regular promissory note and an electronic promissory note?

The primary difference between “regular” (i.e. paper) promissory notes and electronic promissory notes (eNotes) is their format. A regular note is a physical document requiring wet ink signatures, and manual printing, shipping, and storage. It's also vulnerable to loss or damage.An eNote, however, is fully digital—created, signed, executed, and transferred electronically. It does not need printing or physical storage, can't be lost or damaged, and is innately more secure than paper promissory notes.

Q: What does an electronic mortgage note (eNote) include?

An eNote includes all of the same key terms found on a paper note (the loan amount, interest rate, and other payment terms), but will also include information that is unique to eNotes. For example, an eNote will include language that a) identifies it as an eNote and b) indicates that the note is intended for eSignature.Q: Which loans can include an eNote?

There are five factors that determine how digital a loan can be (and if it is eligible to have an eNote). Snapdocs partners with lenders to determine the right digital closing type for each loan in their portfolio—wet, hybrid, eNote, or RON.This tailored approach has helped our customers achieve 2x higher eNote adoption than industry average.